The Valuist Model of Economics

10 August 2022, (2 months ago)

economicsenergyabundancevaluism

Rethinking macro-economics from the viewpoint of energy and time rather than labor and capital.

We need a new system of economics.

In most developed countries today, it is harder for people to meet basic needs like housing, transport, and food than it was 30 years ago. Earning money has become increasingly about power and influence than producing real value. There are many reasons for this tragic failure, I believe the main problem is that current economic ideologies don't care about efficiency, as a result, people’s lives aren't getting easier.

Introducing Valuism

Socialists focus on inequality, capitalists focus on profit, and valuists focus on productivity.

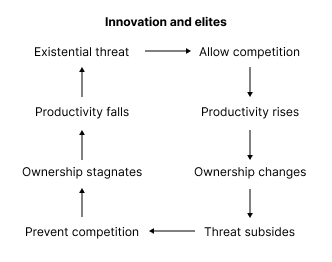

Socialism and capitalism were developed hundreds of years ago for a world where productivity growth didn’t matter. Socialism’s ultimate end is a small elite that plunders the most productive via wealth redistribution under a false pretense of "fairness". Capitalism’s ultimate end is a small elite that plunders the most productive via artificial scarcity under a false pretense of "safety". The problem is that neither system promotes productivity, they focus on capture of productive outputs. Both capitalist and socialist states have risen when competition was encouraged and conversely, decayed when it was prevented.

The elites in both systems only tolerate innovation when they are under-threat and actively prevent it when they aren't. This is because innovation threatens their ownership over productive outputs (a process called creative destruction). It's no surprise that the historic periods with the highest innovation all coincide with the highest periods of inter-state conflict. We need a new “ism” that focuses on productivity growth and doesn’t depend on world wars to accelerate it.

The main difference between prevailing ideologies and Valuism, is that instead of focusing on production inputs like labor or capital, we focus on bottom-line outcomes like people's energy and time. Valuism is directly inspired by the Kardashev Scale but reworked to reflect the impact of knowledge accumulation.

// Feudalism Productivity is dominated by manual labor // Capitalism Productivity is dominated by mechanical production // Valuism Productivity is dominated by applied intelligence

Key principles of Valuism

- The natural state of humanity is poverty.

- Human Life is made of a finite supply of Effort & Time

- Individuals expend Effort & Time to solve their Hierarchy of Problems (starting with survival).

- If something saves Effort & Time or gives individuals more (e.g food), it delivers Value.

- Quality of Life is the number of problems in an individual's Hierarchy of Problems that they can solve. This is roughly the same as the total Value they consume. It is a direct measure of Productivity.

- The overall goal is to maximize Quality of Life by making it easier to produce Value and prevent the destruction of Value.

Derived from Physics

The economy is not a planned construct, it's an emergent system of behavior embedded within other emergent systems. Subatomic particles create physics, atoms create chemistry, molecules create life, and life creates economic systems.

Physics → Chemistry → Biology → Economy

It naturally follows then that economic laws emerge from the laws of the universe.

Power

In physics, energy or work transferred per unit of time is defined as Power.

// Mechanical Power = Work applied per unit of time Power = Work/time

We can similarly define human power as effort transferred per unit of time, where effort is defined as the application of an individual's physical and mental energy.

// Human Power = Effort applied per unit of time Power = Effort/time // Effort definition Effort = Physical Energy + Mental Energy

Productivity

However, it’s easy to put a lot of effort into something completely pointless, an individual’s Effort isn’t necessarily effective. To define Productivity, i.e the actual Value produced, we need a measure of how intelligently that effort is applied. Examples of applied intelligence are things like technical skills or the accumulated knowledge embodied by a tool.

Intelligence = Knowledge of the problem + Knowledge of tools

Thus from a producer’s perspective Value can be defined as follows:

Value Produced = Intelligence ⋅ Effort/time used // Shortened equivalent Value Produced = Intelligence ⋅ Power

From a consumer's point of view, Value is defined as the Energy & Time that having something saves an individual from having to do that thing for themselves.

Value Consumed = Effort/time saved

Bringing it all together

The driving purpose for this whole model is this equation:

Value = Effort/time saved = Intelligence ⋅ Effort/time used // Shortened Value = Human Power Saved = Intelligence ⋅ Human Power Used

As we can see, surplus value comes from the intelligence applied to solving a problem. The intelligence applied in delivering Value adds leverage so that the Effort & Time saved for a consumer is greater than the Effort & Time used to serve them. This is what enables the gains we share by specializing in specific areas and engaging in trade. Instead of trying to solve all our problems ourselves, we benefit from the intelligence of others.

Secondary principles

- Value can be negative, e.g when you force people to spend Effort & Time needlessly

- Price does not necessarily equate to Value, it is influenced by supply and demand

- Hard Money is a stable store of Value, ideally fixed to constant factors of Time & Effort to create any new supply of it (like Gold or Bitcoin).

- Debt is borrowing Value from the future, it is tokenized into a speculative store of Value (like fiat currency).

- Value can grow infinitely despite finite resources, the leverage from applied intelligence makes it possible to consume many times more Value than the amount needed to produce it.

Applying Valuism to Macroeconomics

Prevailing mainstream economic models focus on blunt aggregate metrics like GDP, inflation, and unemployment rates. These measures are vague byproducts of what we actually want to improve. For example, GDP doesn’t reflect tax burdens or productivity at all, if someone steals your car and you’re forced to buy another one, GDP would go up! Similarly, unemployment rates don’t include people that have given up on finding employment, and inflation doesn’t include accommodation, people’s single biggest expense!

Luckily, we can get an idea of the real state of the economy by comparing things that heavily affect people’s energy and time, like median after-tax incomes, prices of basic needs, occupational skills, supply chain costs, energy prices, infrastructure ROI, and regulatory burden. A country that grows in productivity will have people gradually spending a smaller share of their income on basic needs, reflecting increased freedom to focus on their passions instead of survival.

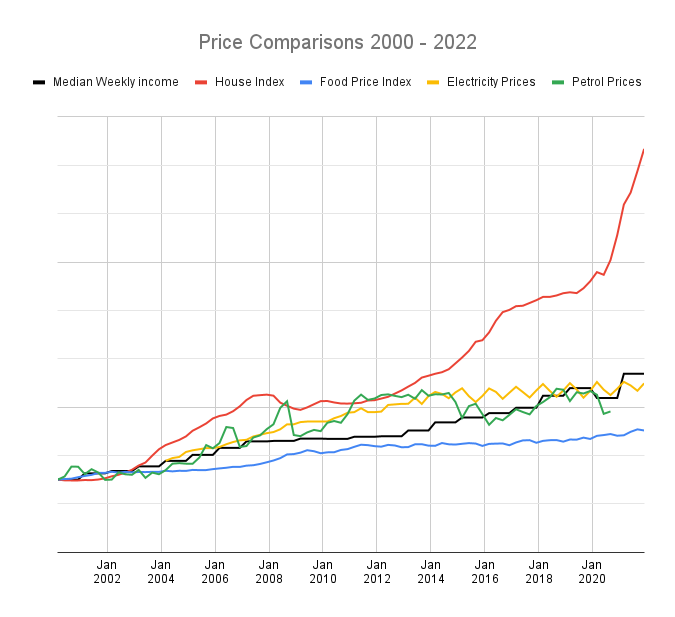

The chart below shows New Zealand’s changes in median incomes relative to the prices of some basic needs since 2000. We can see there was little progress in the first decade of the new Millenium and a serious decline since 2012 driven largely by the cost of housing (via artificial scarcity).

Let’s make a very rough calculation. Assume that in 2000, someone on a median income spent 50% of that income on basic needs with 25% on housing, 15% on food, 7.5% on fuel and 2.5% on electricity. To meet those same basic needs, 75% of the equivalent income today would need to be spent with 57% on housing, 10% on food, 3% on electricity and 6% on fuel.

Practical Example

The other benefit of this theory is that it gives us an easy lens to understand the real impact of everyday decisions. Imagine a series of bad crashes have resulted in pressure to reduce the speed limit on a 250km stretch of road from 100km/h to 80km/h. We can determine if this decision increases Quality of Life by calculating if the time saved by reducing fatalities is greater than the time lost due to the delays from a lower speed.

Assuming Driving Effort & fuel cost etc is unchanged, we need the following annual figures:

Fatality change: 2 deaths/year → 0 deaths per year Travel time change: 2.78 hours → 3.57 hours Average age: 40 Average life expectancy: 80 Total passengers: 600,000

Results:

// Unchanged speed cost: Deaths * (Life expectancy - Average age) = 80 years // Lowering speed cost: Delay * Total passengers = 54 years

From this we can conclude that the speed reduction will result in an increase of Quality of Life in relation to doing nothing as it will save roughly 26 years of life. However, the overall time-cost of using the road is still 244 years of life per annum, several lifetimes!!

Alternative options

If the road could be made to support a 150km/h average speed with zero fatalities, how much value would this unlock?

Using the road currently: Time-expended = 244 years of life per annum Upgraded safely to 150km/hr average speed: Time-expended = 130 years of life per annum

A much larger investment in upgrading the road could free up 6500 years of human productivity over 5 decades whereas a speed reduction will save 1300 years. Improving the road is a better result but this of course depends on whether the resources and expertise are available to do it.

Conclusion

Instead of 18th century ideologies that focus on capture of scarce productive outputs, we need a new creed. One that loves open competition, judges infrastructure and regulations on their ability to increase efficiency above fairness or safety, rewards hi-tech skills, and strives for cheap and abundant raw inputs like food, accommodation, energy and fuel. I think Valuism could form the basis of that creed.

I hope to expand much further on this in the future but I’ll leave it there for now! I would love to know what anyone thinks of this idea 🙂